S&P 500 positive aspects ~1% for the week on Large Tech income spice up; eyes now on Fed meet (SPY)

The S&P 500 (SP500) on Friday added 0.87% for the week to settle at 4,169.48 issues, posting positive aspects in 3 out of 5 periods. Its accompanying SPDR S&P 500 Believe ETF (NYSEARCA:SPY) rose 0.86% for the week.

Sentiment was once helped through robust income from main generation corporations. Then again, positive aspects had been relatively capped through jitters surrounding the regional banking house and financial knowledge that stoked recession worries.

Large Tech took a piece of the highlight this week. FAANG individuals Alphabet (GOOG) (GOOGL) and Meta Platforms (META) inspired with their effects, particularly the latter which noticed its inventory pop just about 14%. The Google-owner beat on each most sensible and final analysis and boosted its proportion buyback, whilst the Fb-parent blew previous promoting income expectancies and touted its paintings on synthetic intelligence.

In the meantime, Microsoft (MSFT) and Intel’s (INTC) experiences had been additionally cheered. The previous noticed its inventory bounce greater than 7% after analysts heaped reward on its Azure cloud unit’s efficiency, whilst the latter equipped outlook that signaled the PC downturn may well be nearing an finish.

The only destructive spot was once Amazon (AMZN), stocks of which erased a post-earnings acquire following a caution on cloud expansion.

Out of doors of Large Tech, the week additionally noticed experiences from well known names similar to the arena’s greatest parcel supply company UPS (UPS), commercial conglomerates 3M (MMM) and GE (GE), telecom massive Verizon (VZ), airplane maker Boeing (BA) and automaker Normal Motors (GM). Subsequent week the income season will see bulletins from Apple (AAPL), Complex Micro Gadgets (AMD), Qualcomm (QCOM), Ford (F) and Starbucks (SBUX), amongst others.

A incessantly worsening scenario at First Republic Financial institution (FRC) additionally took a piece of the highlight this week, reigniting considerations over the stableness of the monetary device. The lender on Monday disclosed over $70B of deposit outflows in its first quarter, sending its inventory plummeting on Tuesday.

The saga additional deepened after a document mentioned the White Space, the Federal Reserve and the Treasury had been bearing in mind plans to avoid wasting the financial institution. This was once adopted through some other document which mentioned FRC was once weighing promoting as much as $100B of securities and mortgages. In any case, on Friday, FRC was once mentioned to be heading for an impending regulatory takeover. The inventory has shed a whopping 75.4% for the week.

The banking worries, in conjunction with knowledge all the way through the week that endured to turn main indicators of cooling within the U.S. economic system, have ended in marketplace individuals bolstering their expectancies that the Fed could be as regards to finishing its rate-hiking marketing campaign.

Leader some of the financial knowledge was once the preliminary estimate for first quarter U.S. GDP which confirmed a acquire of one.1%, considerably not up to the two.6% expansion noticed within the fourth quarter of 2022. Then again, on Friday, the core private intake expenditure index – a key inflation gauge monitored through the Fed – got here in unchanged for March from February, in an indication that inflation was once moderating.

All eyes shall be at the Fed subsequent week, with its financial coverage committee assembly scheduled to finish on Wednesday. Consistent with the CME FedWatch instrument, markets are actually pricing in a ~80% likelihood of a 25 foundation level hike.

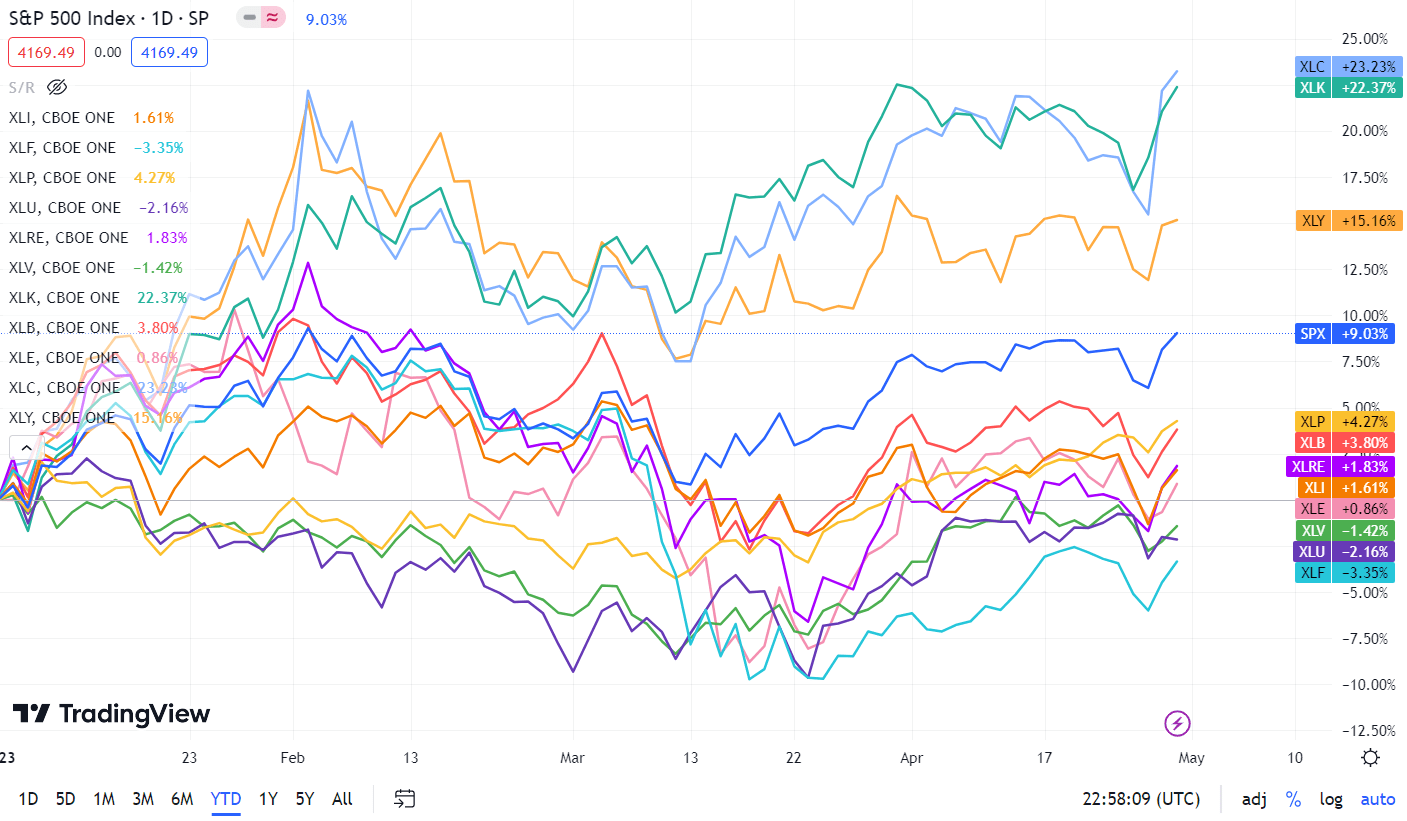

Turning to the weekly efficiency of the S&P 500 (SP500) sectors, six ended within the inexperienced, unsurprisingly led through Conversation Products and services and Generation. Utilities and Industrials crowned the weekly losers. See under a breakdown of the weekly efficiency of the sectors in addition to their accompanying SPDR Make a choice Sector ETFs from April 21 as regards to April 28 shut:

#1: Conversation Products and services +3.76%, and the Conversation Products and services Make a choice Sector SPDR Fund (XLC) +3.83%.

#2: Data Generation +2.43%, and the Generation Make a choice Sector SPDR ETF (XLK) +2.08%.

#3: Actual Property +1.50%, and the Actual Property Make a choice Sector SPDR ETF (XLRE) +1.53%.

#4: Client Staples +1.07%, and the Client Staples Make a choice Sector SPDR ETF (XLP) +1.14%.

#5: Power +0.29%, and the Power Make a choice Sector SPDR ETF (XLE) +0.18%.

#6: Client Discretionary +0.17%, and the Client Discretionary Make a choice Sector SPDR ETF (XLY) +0.33%.

#7: Financials -0.17%, and the Monetary Make a choice Sector SPDR ETF (XLF) -0.15%.

#8: Fabrics -0.19%, and the Fabrics Make a choice Sector SPDR ETF (XLB) -0.19%.

#9: Well being Care -0.59%, and the Well being Care Make a choice Sector SPDR ETF (XLV) -0.57%.

#10: Industrials -0.63%, and the Commercial Make a choice Sector SPDR ETF (XLI) -0.61%.

#11: Utilities -0.99%, and the Utilities Make a choice Sector SPDR ETF (XLU) -0.92%.

Underneath is a chart of the 11 sectors’ YTD efficiency and the way they fared towards the S&P 500. For buyers taking a look into the way forward for what is taking place, check out the In quest of Alpha Catalyst Watch to peer subsequent week’s breakdown of actionable occasions that stand out.