If Hobby Charges Stay Top from 2022 to 2032, Conservative Singaporean Traders to Have the benefit of Bond Making an investment – Cullen Roche

Cullen Roche sat down with Stig Brodersen to talk about how you can body Macro Making an investment into your monetary making plans framework on the We Find out about Billionaires podcast.

There are some gemstones within the interview as a result of Cullen understands worth making an investment and macroeconomics however has spent his profession in wealth control in a monetary making plans way. I’m positive as a result of he wishes to give an explanation for complicated macro-concepts to his previous shoppers in an comprehensible way, he has some excellent analogies to explain some of these things.

Within the interview, Cullen was once requested if we input a duration of emerging rates of interest for many years as an alternative of falling, does this impact how we have a look at bonds. I believed Cullen’s reaction was once beautiful insightful, so I made up our minds to rephrase and checklist it right here.

The Enchantment of Proudly owning Bonds Grow to be Extra Horny As of late Regardless of the Uncertainty

We will purchase six and twelve-month treasury expenses now at a 4% yield, a global that didn’t exist within the ultimate ten to 15 years. With a six-month invoice, you’ll get a one-time coupon. The invoice is not going to do anything else for 6 months, however you’ll recoup at main worth. You simply have to attend and let the invoice seize the go back.

The chance you face when the marketplace rate of interest is at 4% could be very other from when the speed is at 0%.

Many of us consider bonds and the Nineteen Seventies and suppose that bonds have been horrible investments for the reason that rate of interest went up such a lot. The thrilling factor about bonds is the extra rates of interest pass up, you’ll generate extra vital revenue from the brand new bonds you’ll roll your matured bonds into.

For instance, purchasing a bond generates a nominal go back of 8%, and inflation is at 8%. The rate of interest has to proceed to skyrocket much more for the reason that rate of interest has to outpace an excessively prime 8% inflation.

If you happen to personal a 5-year bond, the bond’s length, which measures the bond’s sensitivity to rate of interest fluctuation, is 5 years. When the marketplace rate of interest is going up through 1%, you lose 5% at the worth of your 5-year bond.

When that occurs, you lose your whole coupons earned in the once a year 12 months because of the upward push out there rate of interest for the reason that loss in bond worth is the same as the 5% coupon price paid out to you. But when any person buys your 5-year bond (which has a 5-year length) when your bond’s yield-to-maturity is at 10%, that new bond proprietor must lose bond worth identical to 2 years of bond coupon to lose cash on that bond. The brand new bond proprietor’s chance of a poorer funding consequence diminishes because the bond he purchased is extra horny.

On this regard, bonds perform so much like shares in that once the marketplace rate of interest rises, the costs of present bonds fall, however the long term returns of the prevailing bonds grow to be higher.

The inventory marketplace has a tendency to serve as in a similar fashion. When the inventory marketplace falls in worth, your present inventory funding (as a basket) has a tendency to grow to be the next return-generating tool sooner or later.

The place we’re presently, if rates of interest proceed to jump, you’ll proceed to incur main losses in your present bonds. However the math is now hugely stepped forward for you as a result of you’ll purchase bonds yielding 5%, or 6%, so your start line is far better safe on this global than when the marketplace rate of interest is at 0%.

Many argue that bonds are lifeless and pointless in a style portfolio. There are legitimate arguments about its deficient worth proposition two or 3 years in the past, however these days the maths is totally reworking.

Bonds are a long way awesome these days as a result of marketplace rates of interest have risen, and the chance that rates of interest will proceed to upward push on the present tempo, in Cullen’s opinion, is decrease. This makes bonds much more horny going ahead.

Your Bond Allocation Must be Extremely Personalised

Everyone shouldn’t personal bonds, and no longer everyone wishes those non permanent tools that offer walk in the park over a particular time horizon.

Whether or not you will have to personal bonds will have to be very customized and custom designed. We will have to all glance to construct private and systematic fixed-income portfolios in line with our time horizons.

The dynamics of proudly owning 30-year, 5-month or 5-year bonds/expenses are completely other. It is very important personal bonds in line with the particular time horizon inside your monetary plan, the place you realize the mathematical results that can most likely occur from a nominal viewpoint.

If you happen to personal a 30-year treasury bond, you take on a loopy quantity of 30-year bond length chance, while you might want the cash a lot faster. (For extra in this, you’ll check with my article on How does a Bond Index Fund Recuperate its Price After being Decimated through Emerging Charges?)

Cullen thinks other people will have to no longer have a look at bonds as actual go back coverage. Because of this he’s no longer an actual fan of owing TIPS or inflation-protecting securities within the fixed-income markets.

Bonds will have to be principally main coverage tools that offer main balance over an excessively particular duration.

For instance, the treasury invoice you purchased these days at 4% has no likelihood of thrashing the inflation price, however that isn’t the function of the tool. The function of that bond tool is to come up with a 4% nominal walk in the park as an alternative of having 0% in case you let the cash sit down within the financial institution. The bond is a no brainer to possess IF you have got a six-month time horizon.

Construct a Bond Ladder as Your Bond Allocation

Cullen’s viewpoint about bonds in a portfolio isn’t the preferred go back in step with unit chance optimization defined within the Trendy portfolio method. He approaches it from the viewpoint of getting cash for a particular time horizon when wanted so to have a better walk in the park to fulfill positive liabilities in existence.

This comes from a liability-driven making an investment (LDI) or asset-liability matching method.

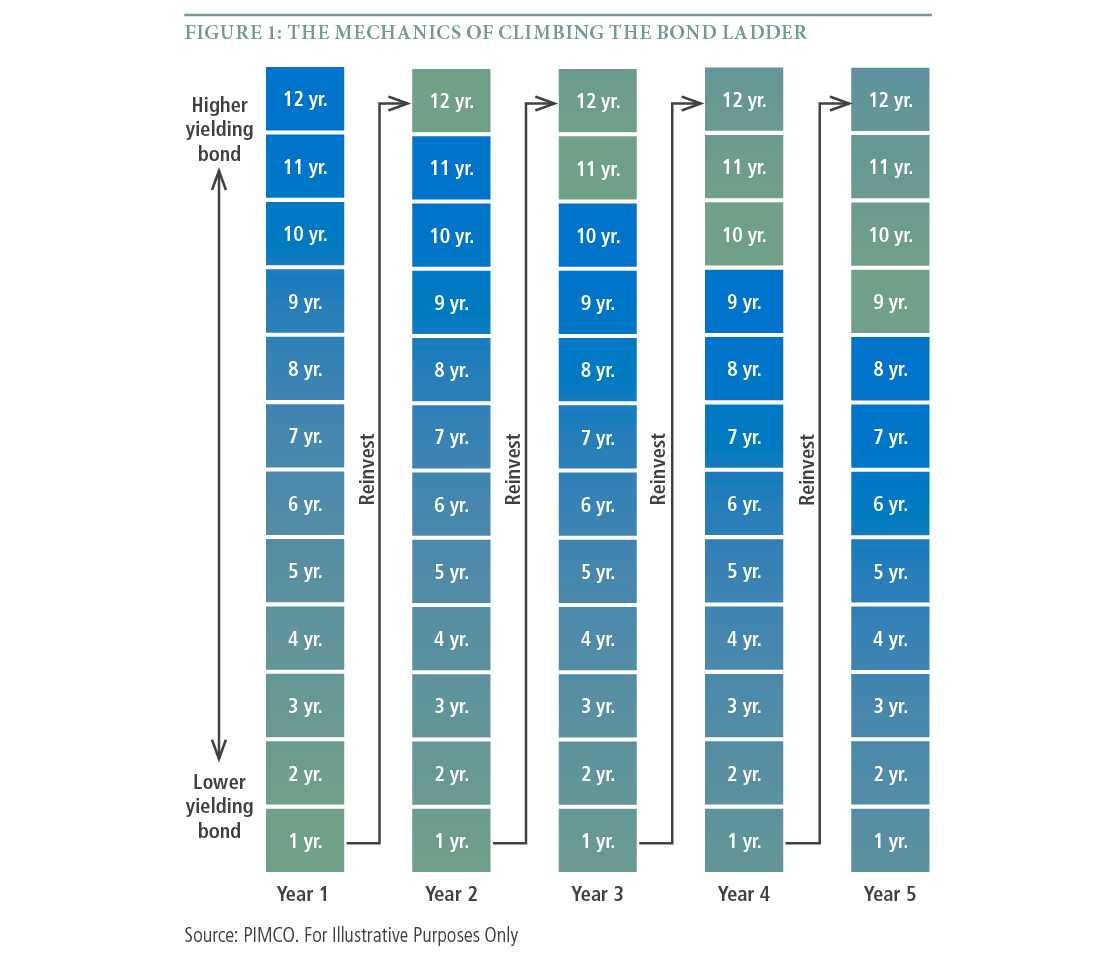

He likes construction bond ladders in a scientific fixed-income portfolio.

For instance, you’ll divide $100,000 into ten parts. Take $10,000 and bucket out with ten bonds that mature from one to 10 years. Annually, one of the crucial bonds to your portfolio will mature, and you’ll systematically roll them over to a brand new set of bonds.

You would not have to care concerning the marketplace rates of interest.

Here’s a visible representation of a 12-year bond ladder from Pimco:

The wonderful thing about a bond ladder is that you’re positive that the primary in your non permanent bucket of cash is there to fulfill your money drift wishes.

If you wish to business those shares I discussed, you’ll open an account with Interactive Agents. Interactive Agents is the main cheap and environment friendly dealer I take advantage of and accept as true with to speculate & business my holdings in Singapore, america, London Inventory Alternate and Hong Kong Inventory Alternate. They mean you can business shares, ETFs, choices, futures, foreign exchange, bonds and finances international from a unmarried built-in account.

You’ll be able to learn extra about my ideas about Interactive Agents in this Interactive Agents Deep Dive Sequence, beginning with how you can create & fund your Interactive Agents account simply.

I invested in a different portfolio of exchange-traded finances (ETF) and shares indexed in america, Hong Kong and London.

My most well-liked dealer to business and custodize my investments is Interactive Agents. Interactive Agents mean you can business in america, UK, Europe, Singapore, Hong Kong and lots of different markets. Choices as neatly. There are not any minimal per thirty days fees, very low foreign exchange charges for forex change, very low commissions for more than a few markets.

To determine extra discuss with Interactive Agents these days.

Sign up for the Funding Moats Telegram channel right here. I can proportion the fabrics, analysis, funding knowledge, offers that I come throughout that permit me to run Funding Moats.

Do Like Me on Fb. I proportion some tidbits that don’t seem to be at the weblog publish there frequently. You’ll be able to additionally make a choice to subscribe to my content material by the use of the e-mail beneath.

I ruin down my assets in line with those subjects:

- Development Your Wealth Basis – If you realize and observe those easy monetary ideas, your longer term wealth will have to be beautiful neatly controlled. In finding out what they’re

- Energetic Making an investment – For lively inventory traders. My deeper ideas from my inventory making an investment enjoy

- Studying about REITs – My Loose “Path” on REIT Making an investment for Newcomers and Seasoned Traders

- Dividend Inventory Tracker – Observe all of the not unusual 4-10% yielding dividend shares in SG

- Loose Inventory Portfolio Monitoring Google Sheets that many love

- Retirement Making plans, Monetary Independence and Spending down cash – My deep dive into how a lot you wish to have to reach those, and the other ways you’ll be financially unfastened

- Providend – The place I lately paintings doing analysis. Rate-Best Advisory. No Commissions. Monetary Independence Advisers and Retirement Consultants. No fee for the primary assembly to know the way it really works

Kyith is the Proprietor and Sole Author at the back of Funding Moats. Readers track in to Funding Moats to be told and construct more potent, less assailable wealth foundations, how you can have a Passive funding technique, know extra about making an investment in REITs and the nuts and bolts of Energetic Making an investment.

Readers additionally observe Kyith to learn to plan neatly for Monetary Safety and Monetary Independence.

Kyith labored as an IT operations engineer from 2004 to 2019. These days, he works as a Senior Answers Specialist in Rate-only Wealth Advisory company Providend.

You’ll be able to view Kyith’s present portfolio right here, which makes use of his Loose Google Inventory Portfolio Tracker.

His funding dealer of selection is Interactive Agents, which permits him to spend money on securities from other exchanges everywhere the arena, at very low fee charges, with out custodian charges, close to spot forex charges.

You’ll be able to learn extra about Kyith right here.