Be Much less Reliant on Banks and Construct More potent Capital Markets by means of Pushing for Higher Shareholder Dividend and Buyback Yield

In BlackRock Chairman and CEO Larry Fink’s 2024 letter to shareholders, he highlighted probably international locations took a peep on the U.S. and wonders what they may be able to do to make themselves extra resilient.

And the important thing could also be to have more potent capital markets:

Final 12 months, I spent numerous days at the highway, logging visits to 17 other international locations. I met with shoppers and staff. I additionally met with many policymakers and heads of state, and throughout the ones conferences, probably the most widespread dialog I had was once concerning the capital markets.

An increasing number of international locations acknowledge the ability of American capital markets and wish to construct their very own.

Of Saudi Arabia, Japan and India:

In Saudi Arabia, for instance, the federal government is serious about development a marketplace for loan securitization, whilst Japan and India wish to give other folks new puts to position their financial savings. These days, in Japan, it’s most commonly the financial institution. In India, it’s regularly in gold.

Once I visited India in November, I met policymakers who lamented their fellow electorate’ fondness for gold. The commodity has underperformed the Indian inventory marketplace, proving a subpar funding for person traders. Nor has making an investment in gold helped the rustic’s financial system.

I believe that in case your inventory marketplace is doing so smartly, then India doesn’t have an identical issues however Larry Fink expands upon this:

Evaluate making an investment in gold with, let’s say, making an investment in a brand new area. While you purchase a house, that creates an financial multiplier impact as a result of you wish to have to furnish and service the home. Perhaps you might have a circle of relatives and fill the home with youngsters. All that generates financial task. Even if somebody places their cash in a financial institution, there’s a multiplier impact since the financial institution can use that cash to fund a loan. However gold? It simply sits in a protected. It may be a just right retailer of worth, however gold doesn’t generate financial expansion.

This can be a small representation — however a just right one — of what international locations wish to accomplish with powerful capital markets. (Or relatively, of what they can’t accomplish with out them.)

Of Japan’s transfer to NISA Financial savings Account:

Final 12 months, Japan handed a demographic milestone. The rustic’s inhabitants has been growing old for the reason that early Nineteen Nineties because the pool of working-age other folks has gotten smaller and the choice of aged has risen. However 2023 was once the primary time that 10% in their other folks exceeded 80 years outdated,6 making Japan the “oldest nation on the earth” in line with the United Countries.7

This is a part of the explanation the Eastern govt is creating a push for retirement funding.

Maximum Eastern stay the majority in their retirement financial savings in banks, incomes a low rate of interest. It wasn’t this kind of dangerous technique when Japan was once affected by deflation, however now the rustic’s financial system has became round, with the NIKKEI surging previous 40,000 for the primary time this month (March 2024).8

Maximum aspiring retirees are lacking out at the upswing. The rustic didn’t have anything else similar to a 401(okay) program till 2001, however even then, the volume of source of revenue other folks may give a contribution was once fairly low. So a decade in the past, the federal government introduced the Nippon Particular person Financial savings Accounts (NISA) to inspire other folks to take a position much more in retirement. Now they’re looking to double NISA’s enrollment. The objective is 34 million Eastern traders earlier than the tip of the last decade.9 It’ll require the Eastern govt to increase their capital markets, which traditionally had little or no retail participation.

Larry Fink spent a while to provide an explanation for concerning the capital markets and why it can be a explanation why US can have bounced again higher:

In finance, there are two elementary tactics to get or develop cash.

One is the financial institution, which is what most of the people traditionally depended on. They deposited their financial savings to earn pastime or took out loans to shop for a house or increase their trade. However over the years a 2nd street for financing arose, in particular within the U.S., with the expansion of the capital markets: Publicly traded shares, bonds, and different securities.

I noticed this firsthand within the overdue Seventies and early Nineteen Eighties after I performed a task within the introduction of the securitization marketplace for mortgages.

Ahead of the Seventies, most of the people secured financing for his or her houses the similar method they did within the Christmas vintage It’s a Glorious Lifestyles — during the Construction & Mortgage (B&L). Shoppers deposited their financial savings into the B&L, which was once necessarily a financial institution. Then that financial institution would flip round and lend out the ones financial savings within the type of mortgages.

Within the film — and in actual existence — the entirety works high-quality till other folks get started lining up on the financial institution’s entrance door asking for his or her deposits again. As Jimmy Stewart defined within the movie, the financial institution didn’t have their cash. It was once tied up in any person else’s area.

After the Nice Despair, B&Ls morphed into financial savings & loans (S&Ls), which had their very own disaster within the Nineteen Eighties. Roughly part of the exceptional house mortgages within the U.S. have been held by means of S&Ls in 1980, and deficient possibility control and unfastened lending practices ended in a raft of disasters costing U.S. taxpayers greater than $100 billion bucks.2

However the S&L disaster didn’t motive the American financial system lasting harm. Why? As a result of on the similar time the S&Ls have been collapsing any other approach of financing was once getting more potent. The capital markets have been offering an street to channel capital again to challenged actual property markets.

This was once loan securitization.

Securitization allowed banks now not simply to make mortgages however to promote them. By means of promoting mortgages, banks may higher arrange possibility on their steadiness sheets and feature capital to lend to house consumers, which is why the S&L disaster didn’t critically affect American homeownership.

Sooner or later, the excesses of loan securitization contributed to the crash in 2008, and in contrast to the S&L disaster, the Nice Recession did hurt house possession within the U.S. The rustic nonetheless hasn’t totally recovered in that appreciate. However the broader underlying development — the growth of the capital markets — was once nonetheless very useful for the American financial system.

Actually, it’s value bearing in mind: Why did the U.S. rebound from 2008 sooner than nearly some other evolved country?3

A large a part of the solution is the rustic’s capital markets.

In Europe, the place maximum property have been stored in banks, economies iced over as banks have been pressured to shrink their steadiness sheets. After all, U.S. banks needed to tighten capital requirements and pull again from lending as smartly. However since the U.S. had a extra powerful secondary pool of cash – the capital markets — the country was once ready to get well a lot more briefly.

These days public equities and bonds supply over 70% of financing for non-financial companies within the U.S. – extra than some other nation on the earth. In China, for instance, the bank-to-capital marketplace ratio is nearly flipped. Chinese language firms depend on financial institution loans for 65% in their financing.4

Individually, that is crucial lesson in fresh financial historical past: Nations aiming for prosperity don’t simply want robust banking techniques — in addition they want robust capital markets.

That lesson is now spreading all over the world.

Many might marvel how digitalisation or fintech goes to weaken conventional financial institution but when the governments are considering what Larry Fink is considering, it’s to effectively advertise a secondary circulate of financial lifeblood to make certain that the multiplier impact doesn’t get killed off simply.

Make the economies much less reliant only on banks.

To be truthful, it isn’t like this isn’t prevalent. We’re listening to lending from different resources however is it identified or executed sufficient to a undeniable level that it prospers?

I’ve at all times view the inventory marketplace as a secondary marketplace to replace possession and due to this fact, I will not know how the inventory marketplace could make other folks rich as opposed to purchasing the inventory at positive level and promoting it, or being paid dividends. Not directly, I at all times puzzled but even so the preliminary public providing, or the rights problems, placements, how does firms thrive.

Till I understand there’s a very robust wealth impact if the inventory marketplace does smartly.

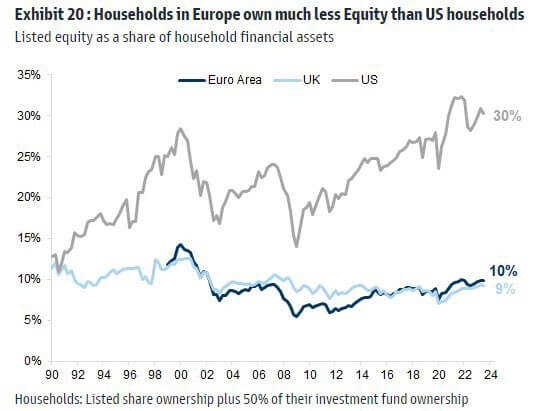

Inventory Possession by means of the inhabitants in the United States is upper and thus when the marketplace does smartly, the inhabitants spend extra.

I occur to return throughout this representation above that displays the United States family possession of equities as a contrarian indicator, however we will take the chance to peer the other ranges of possession.

In Singapore, maximum of our cash is in money & financial savings, belongings and CPF.

As the United States inventory marketplace is so thriving, even firms that have been assume to record of their house nation may be indexed in the United States. You might have firms like Sea Ltd, Spotify record there as a result of they may be able to carry more cash and feature extra consideration.

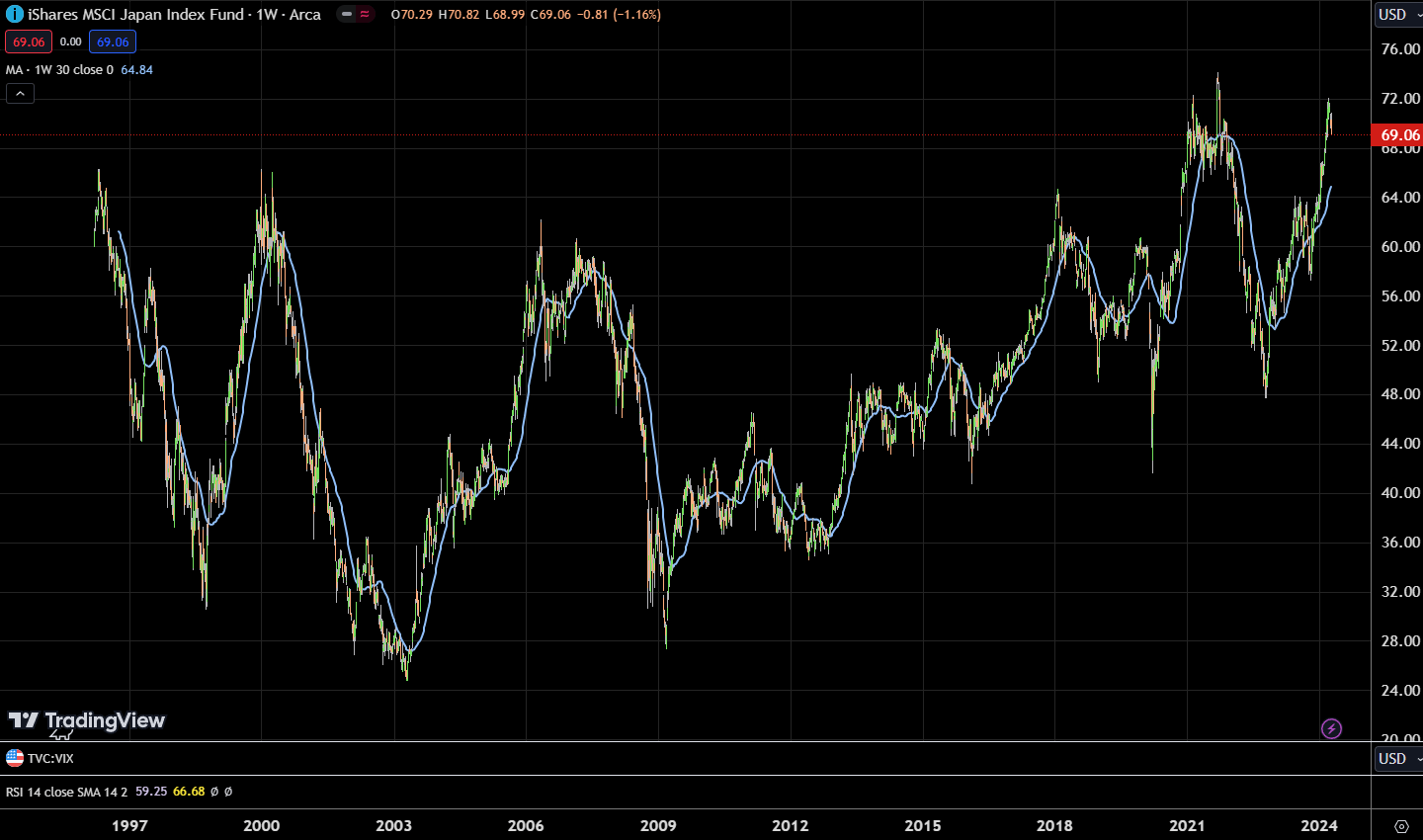

Inventory Marketplace Reform in Japan

However to make your home markets thrive isn’t any simple feat.

They will contain critical reform for your personal public marketplace.

Japan could also be the poster kid. Their markets had been doing smartly previously decade. Unstable however seems to be to be trending up:

Additionally taking part in a task is the Tokyo Inventory Change’s push for firms to spice up their worth, urging managementto run their firms with investor expectancies for returns in thoughts. Companies that want to spend down their money to spice up capital potency are returning cash to shareholders.

Buying and selling area Sojitz, which objectives lifting its marketplace valuation above its e book worth by means of the tip of fiscal 2023, introduced a 16 billion yen percentage buyback in addition to a 5-yen dividend hike in February. Osaka Gasoline has introduced hikes to 72.5 yen this fiscal 12 months and to 95 yen in fiscal 2024.

A number of firms with price-to-book ratios beneath 1 have unveiled buyback plans. Honda Motor introduced a 50 billion yen percentage buyback remaining month after already repurchasing round 200 billion yen in inventory previous this fiscal 12 months.

“We’ll boost up our efforts to toughen capital potency with an eye fixed towards elevating our company worth,” Leader Monetary Officer Eiji Fujimura stated.

Overall shareholder yield as a share of web benefit seems to be set to hit 54%, down 2 issues from fiscal 2022, as profits are rising sooner than returns.

Japan nonetheless lags the U.S. and Europe, with firms within the S&P 500 and Stoxx 600 returning just about 100% and slightly below 80% of web earnings to traders, respectively, QUICK-FactSet knowledge displays. Nonfinancial firms in Japan had a record-high overall of about 106 trillion yen in money readily available on the finish of remaining 12 months, and might face power to make use of it for shareholder returns.

What’s the proper go back to shareholders?

Kyith will argue it’s loose money drift yield. However increasingly, buybacks is being checked out as a type of go back. Corporations are extra assured to pay out dividends and buyback their percentage in the event that they really feel that they have got cash to spend.

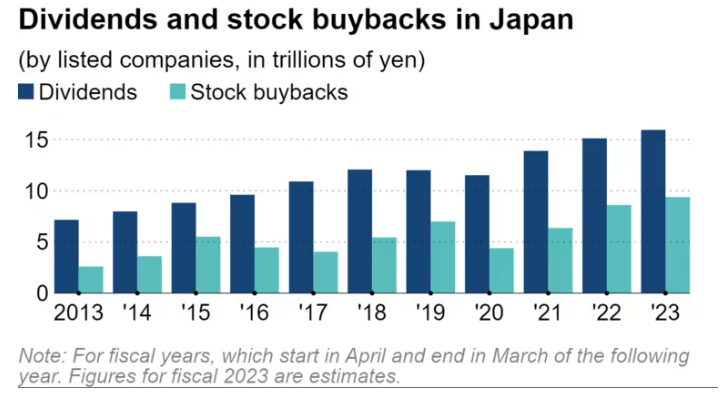

So the buyback + dividend yield, or what Japan phrases as payouts to shareholders, is an effective way to take a look at shareholder returns:

Payouts to shareholders by means of indexed firms in Japan are anticipated to succeed in an all-time excessive of about 25 trillion yen ($165 billion) for the fiscal 12 months finishing this month, amid rising profits in addition to power to make use of capital extra successfully.

The overall, which contains dividends and percentage repurchases, was once calculated by means of Nikkei from 2,300 firms that shut their books in March. The dividends are in accordance with QUICK Consensus analyst forecasts for firms that experience now not equipped estimates, and account for inventory splits and opposite inventory splits. The buybacks quilt delicate gives and plans disclosed since remaining April.

Dividends are set to develop 6% to about 15.9 trillion yen, and repurchases by means of 9% to 9.3 trillion yen, each listing highs. A complete of 360 firms have raised their deliberate dividends for the reason that finish of 2023, including about 200 billion yen to the entire payout, and percentage buyback plans value 1.42 trillion yen had been introduced since January.

The upward thrust in returns will get advantages retail traders, who’re being inspired to take part within the inventory marketplace thru channels such because the remodeled Nippon Particular person Financial savings Account tax-exempt funding program.

Folks now personal about one-fifth of all indexed stocks in Japan. In accordance with those figures, more or less 3 trillion yen in dividends by myself would move to families, an identical to about 0.5% of Japan’s gross home product.

In Arcus Funding Insights December 2023, Peter Tasker indexed 5 becoming eventualities for the 12 months of the dragon. They’re Japan-oriented. One level talks concerning the NISA and the way it will get advantages Japan shares:

I might argue that Japan is reasonably in the back of time in this. The larger affect is the reforms the change is pushing to make shareholder returns extra interesting and, due to this fact, making participation upper.

That is what Japan is doing significantly better than Singapore.

What has this were given to do with Singapore?

I will be able to see some minister or some bizarre taskforce being created and a few deficient student is tasked to try having a just right 2nd engine to the banking device. In the event that they deem that that is wanted and there’s sufficient make stronger, there could also be an enormous push.

There’s community results in a market.

You’re going to want the firms to be valued and traded successfully. Public crowd wishes to wish the shares sufficient.

However to do #1, you wish to have to turn visual shareholder returns, and generally this is within the type of buyback and dividends. Corporations want to lead them to extra horny.

In Asia, there’s numerous historically circle of relatives firms that experience their very own schedule as opposed to the shareholders.

It’s for the federal government and change to take a look at and alter that.

Equities if stay undervalue could also be revalue to what they’re value in the end when that occurs. The query is when that may occur and I’m afraid impatient Millennial, Gen X or Gen Z traders would now not chunk.

Equities is an extended sport that to seize the worth, it’s possible you’ll want to grasp twenty years. Thus, handiest the ones with deep wallet and with endurance will probably be rewarded. However the firms will have to be value one thing.

I invested in a various portfolio of exchange-traded finances (ETF) and shares indexed in the United States, Hong Kong and London.

My most popular dealer to business and custodize my investments is Interactive Agents. Interactive Agents assist you to business in the United States, UK, Europe, Singapore, Hong Kong and plenty of different markets. Choices as smartly. There are not any minimal per thirty days fees, very low foreign exchange charges for forex change, very low commissions for more than a few markets.

Sign up for the Funding Moats Telegram channel right here. I will be able to percentage the fabrics, analysis, funding knowledge, offers that I come throughout that permit me to run Funding Moats.

Do Like Me on Fb. I percentage some tidbits that aren’t at the weblog publish there regularly. You’ll be able to additionally make a choice to subscribe to my content material by way of the e-mail beneath.

I spoil down my assets in line with those subjects:

Construction Your Wealth Basis – If you understand and observe those easy economic ideas, your long run wealth will have to be lovely smartly controlled. To find out what they’re

Energetic Making an investment – For energetic inventory traders. My deeper ideas from my inventory making an investment revel in

Studying about REITs – My Loose “Direction” on REIT Making an investment for Inexperienced persons and Seasoned Buyers

Providend – The place I used to paintings doing analysis. Charge-Simplest Advisory. No Commissions. Monetary Independence Advisers and Retirement Experts. No price for the primary assembly to know how it really works

Havend – The place I these days paintings. We want to ship commission-based insurance coverage recommendation in a greater method.

Kyith is the Proprietor and Sole Author in the back of Funding Moats. Readers track in to Funding Moats to be informed and construct more potent, more impregnable wealth foundations, learn how to have a Passive funding technique, know extra about making an investment in REITs and the nuts and bolts of Energetic Making an investment.

Readers additionally observe Kyith to learn to plan smartly for Monetary Safety and Monetary Independence.

Kyith labored as an IT operations engineer from 2004 to 2019. These days, he works as a Senior Answers Specialist in Insurance coverage Get started-up Havend. All reviews on Funding Moats are his personal and does now not constitute the perspectives of Providend.

His funding dealer of selection is Interactive Agents, which permits him to put money into securities from other exchanges in every single place the arena, at very low fee charges, with out custodian charges, close to spot forex charges.

Risk Warning: 74-89% of retail investor accounts lose money when trading CFDs . You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money