Couple who need a easy retirement fear inflation will harm plans

John is afraid inflation will devour away such a lot of his pension the couple will simplest have sufficient for groceries

Evaluations and proposals are impartial and merchandise are independently decided on. Postmedia would possibly earn an associate fee from purchases made thru hyperlinks in this web page.

Article content material

John* is able to retire and now not glance again. The programming analyst has constructed his occupation with the government over the last 33 years and plans to retire on the finish of this 12 months.

Commercial 2

Article content material

“I’m 62 years outdated and I’m carried out with paintings, however I fear that inflation will devour away at my pension till it’s simplest sufficient for groceries.”

Article content material

John these days earns about $90,000 a 12 months prior to tax (about $60,000 after tax). His executive defined-benefit 401-k plan is listed to inflation and can pay $62,000 a 12 months prior to tax if he retires as deliberate this 12 months. A part of the pension is a bridged advantage to approximate Canada Pension Plan (CPP) bills till age 65.

Article content material

His spouse Cathy is 55 and works within the personal sector. Her annual source of revenue is set $60,000 prior to tax. She plans to paintings some other 5 to 8 years prior to retiring. Her employer transformed their as soon as defined-benefit 401-k plan to a defined-contribution plan, so she used a part of that cash ($68,000) to buy a automobile and put the remaining in a locked-in retirement plan.

Commercial 3

Article content material

“It would take a little time to pay again the pension cash used to shop for the automobile,” John stated.

Every of them has about $60,000 in a registered retirement financial savings plan (RRSP) invested in moderate-risk mutual budget. They personal a single-family house in Ottawa price about $500,000, however don’t have a loan or some other giant money owed. John estimates their present per thirty days bills run about $3,500 with the excess source of revenue going into the financial institution and to “repay” the pension cash used to buy the automobile.

My fundamental imaginative and prescient for retirement is that I forestall running. I’ve quite simple wishes

John

The couple reside modestly and haven’t any giant plans for retirement rather then to pursue private pursuits, so long as there’s sufficient cash to take action.

“My fundamental imaginative and prescient for retirement is that I forestall running. I’ve quite simple wishes,” John stated. “I wish to discover ways to play guitar. We don’t have any giant shuttle plans in thoughts. It could be great in an effort to have the funds for to shuttle, whether or not we do or now not, is a special factor. Our ultimate commute was once to Disney Global again in 2000.”

Article content material

Commercial 4

Article content material

The couple don’t have youngsters, however they want to depart cash to their nieces and nephews.

In the event that they have been to splurge, they’d like to buy a swim spa, which will require some house renovations so it might be used year-round. John estimates it will value between $80,000 and $100,000 and they might take out a loan on their space to do it. That stated, their greatest precedence is to make sure they’re relaxed in retirement.

“Is that this going to paintings?” he requested.

What the mavens say

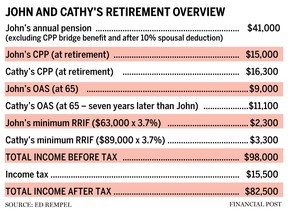

According to the numbers supplied and their desired way of life, John and Cathy can each retire lately, Ed Rempel, a fee-for-service monetary planner, tax accountant and blogger, stated.

“Their present way of life bills are about $3,500 a month, or $42,000 a 12 months, which will require an source of revenue of $46,000 a 12 months prior to tax,” he stated. John’s pension by myself is greater than this.”

Commercial 5

Article content material

Eliott Einarson, a retirement planner at Ottawa-based Exponent Funding Control, has the same opinion.

“I see this so much in my very own follow. Individuals are searching for readability on what’s conceivable,” he stated. “They’re debt loose and John’s pension plus CPP and OAS (Previous Age Safety) when he claims them will most likely come on the subject of his present internet source of revenue. They’re high quality.”

However Rempel is worried they haven’t regarded as all their doable spending wishes, akin to leisure, scientific bills, items, and so on.

“I added an extra $2,500 a 12 months for scientific bills assuming any well being advantages forestall when he retires, $5,000 for holidays and a $68,000 automobile each and every 10 years, assuming they wish to stay a identical automobile to what they’ve and pressure it for a very long time,” he stated. “This quantities to $56,000 a 12 months — $64,000 prior to tax — or $4,700 a month to spend to succeed in their desired retirement way of life.”

Commercial 6

Article content material

He recommends they take a better take a look at the additional cash (about $2,200) they’ve coming in each and every month. At the moment, it’s now not transparent the place it’s going. In the event that they do not anything with it, they’ll slowly begin to spend extra and it’s going to grow to be a part of their way of life spending.

Rempel recommends John break up $18,000 of his pension with Cathy so they are able to each be within the lowest tax bracket. This may save $1,500 a 12 months and make sure their OAS bills is probably not clawed again.

“Each will have to convert their RRSPs to a registered retirement source of revenue fund and a lifestyles source of revenue fund, and get started taking the minimal withdrawal when Cathy retires at 63 and John is 70,” he stated.

As for when to assert CPP advantages, Rempel stated the highest two concerns are funding returns and tax.

Commercial 7

Article content material

“Since they put money into balanced mutual budget, their charge of go back will have to be very similar to CPP, about 5 in line with cent a 12 months,” he stated. “They’ll almost definitely pay much less tax if they begin John’s CPP and OAS at age 70 when Cathy retires, and Cathy’s CPP at 63 when she retires and OAS on the earliest age of 65.”

Relying on its price, Einarson stated it’s going to make sense not to take the pension bridge John has get entry to to and as a substitute use his RRSP to conquer any gaps till he claims CPP, however the swim spa is definitely inside their succeed in.

“Retirement is set coins movement. If bills are simplest about $3,500, they may take out a line of credit score or a loan and with ease paintings that value into their cash-flow wishes,” he stated. “It’s very potential, specifically if Cathy goes to proceed running for the following seven to 8 years. They may make sure that the swim spa reno is paid off by the point she retires to really feel an extra little bit of protection.”

Commercial 8

Article content material

Einarson added that in the event that they psychologically don’t thoughts having debt, they may take out a longer-term loan to repay the spa prematurely.

He additionally recommends making an investment their surplus source of revenue within tax-free financial savings accounts.

“They’re a super financial savings instrument for the couple in the event that they do want further budget and likewise to increase cash for the property, which they may depart to their nieces and nephews,” he stated.

*Names had been modified to give protection to privateness.

_____________________________________________________________

For those who like this tale, join the FP Investor Publication.

_____________________________________________________________

Feedback

Postmedia is dedicated to keeping up a full of life however civil discussion board for dialogue and inspire all readers to percentage their perspectives on our articles. Feedback would possibly take as much as an hour for moderation prior to showing at the website online. We ask you to stay your feedback related and respectful. We’ve got enabled electronic mail notifications—you’ll now obtain an electronic mail if you happen to obtain a answer for your remark, there may be an replace to a remark thread you observe or if a consumer you observe feedback. Talk over with our Neighborhood Tips for more info and main points on learn how to modify your electronic mail settings.

Sign up for the Dialog