2022 2023 Tax Brackets, Same old Deduction, Capital Positive factors, and so forth.

My different submit indexed 2022 2023 401k and IRA contribution and source of revenue limits. I additionally calculated the inflation-adjusted tax brackets and one of the crucial maximum frequently used numbers in tax making plans for 2023 the use of the printed inflation numbers and the similar formulation prescribed within the tax legislation. The respectable numbers introduced by means of the IRS showed my calculations.

2022 2023 Same old Deduction

You don’t pay federal source of revenue tax on each and every buck of your source of revenue. You deduct an quantity out of your source of revenue prior to you calculate taxes. About 90% of all taxpayers take the usual deduction. The opposite ~10% itemize deductions when their general deductions exceed the usual deduction. In different phrases, you’re deducting a bigger quantity than your allowed deductions when you’re taking the usual deduction. Don’t really feel dangerous about taking the usual deduction!

The fundamental same old deduction in 2022 and 2023 are:

| 2022 | 2023 | |

|---|---|---|

| Unmarried or Married Submitting One at a time | $12,950 | $13,850 |

| Head of Family | $19,400 | $20,800 |

| Married Submitting Collectively | $25,900 | $27,700 |

Supply: IRS Rev. Proc. 2021-45, Rev. Proc. 2022-38.

People who find themselves age 65 and over have the next same old deduction than the elemental same old deduction.

| 2022 | 2023 | |

|---|---|---|

| Unmarried, age 65 and over | $14,700 | $15,700 |

| Head of Family, age 65 and over | $21,150 | $22,650 |

| Married Submitting Collectively, one individual age 65 and over | $27,300 | $29,200 |

| Married Submitting Collectively, each age 65 and over | $28,700 | $30,700 |

Supply: IRS Rev. Proc. 2021-45, Rev. Proc. 2022-38.

People who find themselves blind have an extra same old deduction.

| 2022 | 2023 | |

|---|---|---|

| Unmarried or Head of Family, blind | +$1,750 | +$1,850 |

| Married Submitting Collectively, one individual is blind | +$1,400 | +$1,500 |

| Married Submitting Collectively, each are blind | +$2,800 | +$3,000 |

Supply: IRS Rev. Proc. 2021-45, Rev. Proc. 2022-38.

2022 2023 Tax Brackets

The tax brackets are in keeping with taxable source of revenue, which is AGI minus more than a few deductions. The tax brackets in 2022 are:

| Unmarried | Head of Family | Married Submitting Collectively | |

|---|---|---|---|

| 10% | $0 – $10,275 | $0 – $14,650 | $0 – $20,550 |

| 12% | $10,275- $41,775 | $14,650 – $55,900 | $20,550 – $83,550 |

| 22% | $41,775 – $89,075 | $55,900 – $89,050 | $83,550 – $178,150 |

| 24% | $89,075 – $170,050 | $89,050 – $170,050 | $178,150 – $340,100 |

| 32% | $170,050 – $215,950 | $170,050 – $215,950 | $340,100 – $431,900 |

| 35% | $215,950 – $539,900 | $215,950 – $539,900 | $431,900 – $647,850 |

| 37% | Over $539,900 | Over $539,900 | Over $647,850 |

Supply: IRS Rev. Proc. 2021-45.

The 2023 tax brackets are:

| Unmarried | Head of Family | Married Submitting Collectively | |

|---|---|---|---|

| 10% | $0 – $11,000 | $0 – $15,700 | $0 – $22,000 |

| 12% | $11,000 – $44,725 | $15,700 – $59,850 | $22,000 – $89,450 |

| 22% | $44,725 – $95,375 | $59,850 – $95,350 | $89,450 – $190,750 |

| 24% | $95,375 – $182,100 | $95,350 – $182,100 | $190,750 – $364,200 |

| 32% | $182,100 – $231,250 | $182,100 – $231,250 | $364,200 – $462,500 |

| 35% | $231,250 – $578,125 | $231,250 – $578,100 | $462,500 – $693,750 |

| 37% | Over $578,125 | Over $578,100 | Over $693,750 |

Supply: IRS Rev. Proc. 2022-38.

A commonplace false impression is that while you get into the next tax bracket, all of your source of revenue is taxed on the upper fee, and also you’re at an advantage now not having the additional source of revenue. That’s now not true. Tax brackets paintings incrementally. For those who’re $1,000 into the following tax bracket, best $1,000 is taxed on the upper fee. It doesn’t have an effect on the source of revenue within the earlier brackets.

For instance, any individual unmarried with a $60,000 AGI in 2022 can pay:

| First 12,950 (the usual deduction) | 0% | ||

| Subsequent $10,275 | 10% | ||

| Subsequent $31,500 ($41,775 – $10,275) | 12% | ||

| Ultimate $5,275 | 22% |

This individual is within the 22% tax bracket however best not up to 10% of the $60,000 AGI is in point of fact taxed at 22%. The majority of the source of revenue is taxed at 0%, 10%, and 12%. The mixed tax fee is best 9.9%. If this individual doesn’t earn the overall $5,275, she or he is within the 12% bracket as an alternative of the 22% bracket, however the mixed tax fee best is going down rather from 9.9% to eight.8%. Making the additional source of revenue doesn’t value this individual extra in taxes than the additional source of revenue.

Don’t be frightened of going into the following tax bracket.

2022 2023 Capital Positive factors Tax

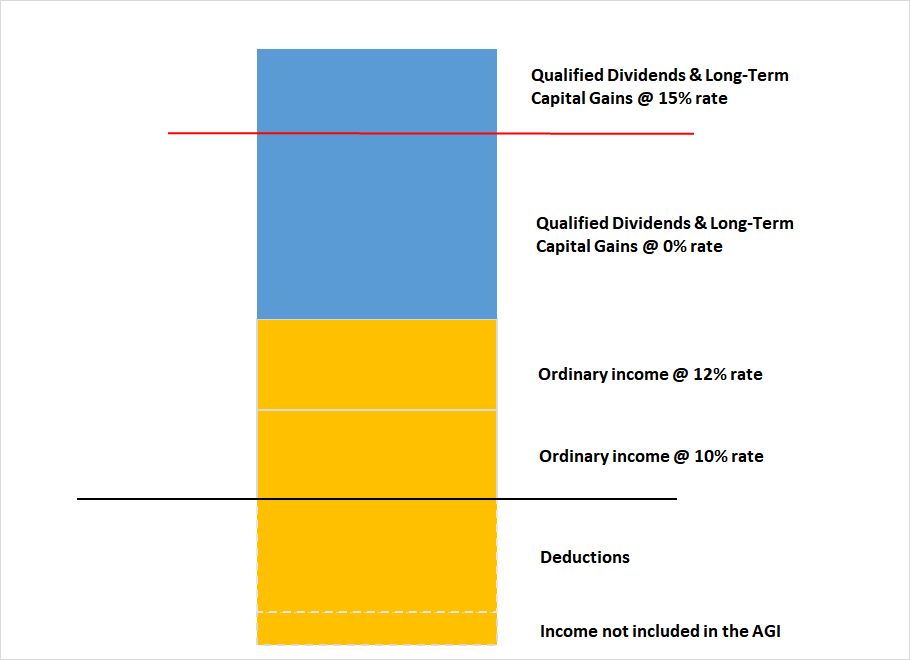

When your different taxable source of revenue (after deductions) plus your certified dividends and long-term capital beneficial properties are under a cutoff, you are going to pay 0% federal source of revenue tax for your certified dividends and long-term capital beneficial properties underneath this cutoff.

That is illustrated by means of the chart under. Taxable source of revenue is the phase above the black line, after subtracting deductions. A portion of the certified dividends and long-term capital beneficial properties is taxed at 0% when the opposite taxable source of revenue plus those certified dividends and long-term capital beneficial properties are underneath the purple line.

The purple line is as regards to the highest of the 12% tax bracket however they don’t line up precisely.

| 2022 | 2023 | |

|---|---|---|

| Unmarried or Married Submitting One at a time | $41,675 | $44,625 |

| Head of Family | $55,800 | $59,750 |

| Married Submitting Collectively | $83,350 | $89,250 |

Supply: IRS Rev. Proc. 2021-45, Rev. Proc. 2022-38.

For instance, assume a married couple submitting collectively has $70,000 in different taxable source of revenue (after deductions) and $20,000 in certified dividends and long-term capital beneficial properties in 2022. The utmost 0 fee quantity cutoff is $83,350. $13,350 of the certified dividends and long-term capital beneficial properties ($83,350 – $70,000) is taxed at 0%. The rest $20,000 – $13,350 = $6,650 is taxed at 15%.

A an identical threshold exists at the higher finish for certified dividends and long-term capital beneficial properties. When your different taxable source of revenue (after deductions) plus your certified dividends and long-term capital beneficial properties are above a cutoff, you are going to pay 20% federal source of revenue tax as an alternative of 15% for your certified dividends and long-term capital beneficial properties above this cutoff.

| 2022 | 2023 | |

|---|---|---|

| Unmarried | $459,750 | $492,300 |

| Head of Family | $488,500 | $523,050 |

| Married Submitting Collectively | $517,200 | $553,850 |

| Married Submitting One at a time | $258,600 | $276,900 |

Supply: IRS Rev. Proc. 2021-45, Rev. Proc. 2022-38.

2022 2023 Property and Agree with Tax Brackets

Estates and trusts have other tax brackets than people. Those practice to non-grantor trusts and estates that retain source of revenue versus distributing the source of revenue to beneficiaries. Grantor trusts (together with the most typical revocable residing trusts) don’t pay taxes one by one. The source of revenue of a grantor accept as true with is taxed to the grantor on the grantor’s tax brackets.

Listed below are the tax brackets for estates and trusts in 2022 and 2023:

| 2022 | 2023 | |

|---|---|---|

| 10% | $0 – $2,750 | $0 – $2,900 |

| 24% | $2,750 – $9,850 | $2,900 – $10,550 |

| 35% | $9,850 – $13,450 | $10,550 – $14,450 |

| 37% | over $13,450 | over $14,450 |

Supply: IRS Rev. Proc. 2021-45, Rev. Proc. 2022-38.

2022 2023 Present Tax Exclusion

Every individual may give someone else as much as a suite quantity in a calendar yr with no need to report a present tax shape. Now not that submitting a present tax shape is laborious, however many of us steer clear of it if they are able to. In 2023, this present tax exclusion quantity will most probably build up from $16,000 to $17,000.

| 2022 | 2023 | |

|---|---|---|

| Present Tax Exclusion | $16,000 | $17,000 |

Supply: IRS Rev. Proc. 2021-45, Rev. Proc. 2022-38.

The present tax exclusion is counted by means of each and every giver to each and every recipient. As a giver, you’ll surrender to $16,000 each and every in 2022 to an infinite selection of folks with no need to report a present tax shape. For those who give $16,000 to each and every of your 10 grandkids in 2022 for a complete of $160,000, you continue to gained’t be required to report a present tax shape. Any recipient too can obtain a present from an infinite selection of folks. If a grandchild receives $16,000 from each and every of his or her 4 grandparents in 2022, no taxes or tax bureaucracy will likely be required.

2022 2023 Financial savings Bonds Tax-Unfastened Redemption for School Bills

For those who money out U.S. Financial savings Bonds (Sequence I or Sequence EE) for varsity bills or switch to a 529 plan, your changed adjusted gross source of revenue should be underneath positive limits to get a tax exemption at the hobby. See Money Out I Bonds Tax Unfastened For School Bills Or 529 Plan. Listed below are the source of revenue limits in 2022 and 2023:

| 2022 | 2023 | |

|---|---|---|

| Unmarried, Head of Family | $85,800 – $100,800 | $91,850 – $106,850 |

| Married Submitting Collectively | $128,650 – $158,650 | $137,800 – $167,800 |

Supply: IRS Rev. Proc. 2021-45, Rev. Proc. 2022-38.

Say No To Control Charges

If you’re paying an consultant a share of your property, you’re paying 5-10x an excessive amount of. Learn to in finding an unbiased consultant, pay for recommendation, and best the recommendation.